When Looking to Finance Higher Education, What is the Best Order to Look for Funding Sources?

Welcome to 2021, where even the most basic entry-level jobs have a degree requirement. However, this reality comes in the face of a rising college education which costs as much as 10,000 dollars a year at a public institution to more than 35,000 dollars at select private colleges.

When looking to finance higher education, the best order to look for funding sources is grants and scholarships first because these come with the assurance of no interest. Next, one can go for federal student loans, which are a good option since the accompanying interest rates are low and fixed.

Out of all the college financing options available, the worst is private loans, which offer high-interest rates and (usually) poor repayment conditions.

The fact of the matter is that post-secondary education is important for the future economic stability of any nation and the individual himself. The disadvantage is the cost, which keeps many middle-income and lower-income students from achieving a degree of their choice.

Suppose you have attended any higher education conference or read a book on the topic of post-secondary education in the United States. In that case, you have most likely come across predictions in the recent past about two out of three jobs requiring a college degree of some sort by 2020.

Statistics such as those highlighted by Georgetown University all seemed to indicate that by 2020, up to 65% of jobs would make post-secondary education a basic requirement. The latest data from 2020 and beyond suggests that up to 70% of workers had a college education by 2018. Compare this to 2010, where only 59% of workers had accompanying degrees.

This in itself is an incentive for education leaders to come up with alternatives to the conventional American college models. The status of post-secondary education shows that the government needs to step in to alleviate the situation.

This post may contain affiliate links. You can read the full disclosure here.

Analysts and economists suggest that the sharp rise in college graduates in recent years is due to the increasing literacy levels in the United States. The same sources have also likened the situation to the Great Recession, where employers had their pick of college graduates to choose. Same as it was back then, employers today opt for potential hires with college degrees.

When making financial plans for college, prospective students should keep in mind the associated costs such as travel, tuition fees, personal expenses, health insurance costs, food, accommodation, visa, and student service fees. Aspiring college students can choose to work with companies like Upromise to save for college and alleviate the financial load.

According to a Financial Literacy and Education Commission (FLEC) report, among the most important decisions college students are faced with daily include how much to work and how to use a bank or credit union account properly.

In addition to this, students also have to quickly learn the ins and outs of student loan rates and how to manage credit cards. For this, a service like UpStart can be helpful. They help students find the best loan rates out there for everything and anything including paying off credit cards, consolidating debt, paying for grad school, expanding a business, and more.

Many will require some form of credit repair before they can begin to source for college financing. The most important lesson for any college student that will last well beyond college is the value of budgeting.

So, when looking to finance higher education, what is the best order to look for funding sources?

Grants and Scholarships

When it comes to funding for college, both scholarships and grants are free guaranteed sources of money to help students pay for their continuing education. Compared to student loans, which you have to pay back, grants and scholarships do not need to be paid back (unless you withdraw from the program early or change your enrollment status).

The main difference between grants and loans is that grants are specifically designed to help needy students pay for their tuition and college expenses. On the other hand, scholarships can be both merit-based and need-based, where they are usually awarded based on a hobby, religion, or even a specific ethnicity.

Types of Grants

- Need-based grants – These are awarded based on the economic situation of your family. To properly assess the level of a student’s economic need, the student must fill out a Free Application for Federal Student Aid (FAFSA), as well as the Expected Family Contribution (EFC) form. In many cases, EFC numbers are used by schools to establish the amount of financial aid that students are eligible to receive.

- Merit-based grants are regularly awarded to students who show a great aptitude for academic achievement while also displaying an unwavering commitment to community service. Qualifying students also exhibit above-par leadership skills, as well as enhanced soft skills. College merit-based grant programs are mostly found by doing refined online searches around one’s home state first.

How to Win Grants for College Tuition

- Ensure you fill out the FAFSA form – this is a form deemed necessary by both the state and federal governments, which provide helpful college grants. Only a FAFSA application can help you qualify and become eligible for such grants. The financial aid received courtesy of such grants goes a long way towards helping needy students cover their college expenses. At the same time, good saving habits are an investment that will last a lifetime, especially for students from disadvantaged backgrounds.

- Make sure you submit the FAFSA way before the required deadline – when filling out grant and scholarship application forms, it is important to remember that they are awarded on a first-come, first-served basis.

- Ensure that you read the financial aid offer that you receive – If you are a good student, you will receive offers from several colleges. Included in the offers is information regarding your eligibility for college grants. Also included in these packages is extra information about other types of financial aid available to you at each college, including work-study, federal student loans, and scholarships.

For wise parents with their children’s futures in mind, an early tax-advantaged investment account specifically tailored for children is a fantastic idea. Programs such as UNest are designed to help you achieve this goal of crafting a better future for your children.

Scholarships

Alternatively, college students can apply for scholarships. Scholarships are a form of financial aid for college students. These are a form of financial aid for college tuition and are available at the local nonprofit level to the federal level.

The great thing about scholarships is that you don’t have to pay them back. These funds are also merit-based, and only your accomplishments and academic record can get you through the door. Common measures used to assess your suitability include volunteer hours, grade point average, and conventional standardized test scores.

There are several scholarships available at select colleges for students with exceptional athletic ability. The catch is that you will have to play a sport for the college during your time there. In most cases, scholarship coverage and information depend on the organization or person offering it.

Some scholarships might be for $500 one time; others might be for $10,000 and renew every year. The important thing is to make sure that you understand all the requirements for qualifying for each scholarship.

Prospective college students need to know that scholarship searches can be as intensive as full-time jobs, especially if one intends to have all their expenses covered by scholarships. The best sites for landing lucrative scholarships include College Board, Fast Web, and Scholarships.com.

While hunting for scholarships, you can drill down by gender, grade point average, military affiliation, financial need, ethnicity, standardized test scores, and disability. The other factors to consider include scholarship type, amount, deadlines, and associated majors.

The most popular types of scholarships to keep in mind include awards based on the field of study for individual students who have already decided what they want to study (major). There are also scholarships for graduate studies, which cater to post-graduate education costs. Hobby-based scholarships are awarded based on activities, skills, and interests, which depend on the individual.

Aside from scholarships and grants, you can opt to hold a job at night to pay your way through college while saving and finding ways to lower your bills.

Lowering your bills is also an effective way of sticking to your budget.

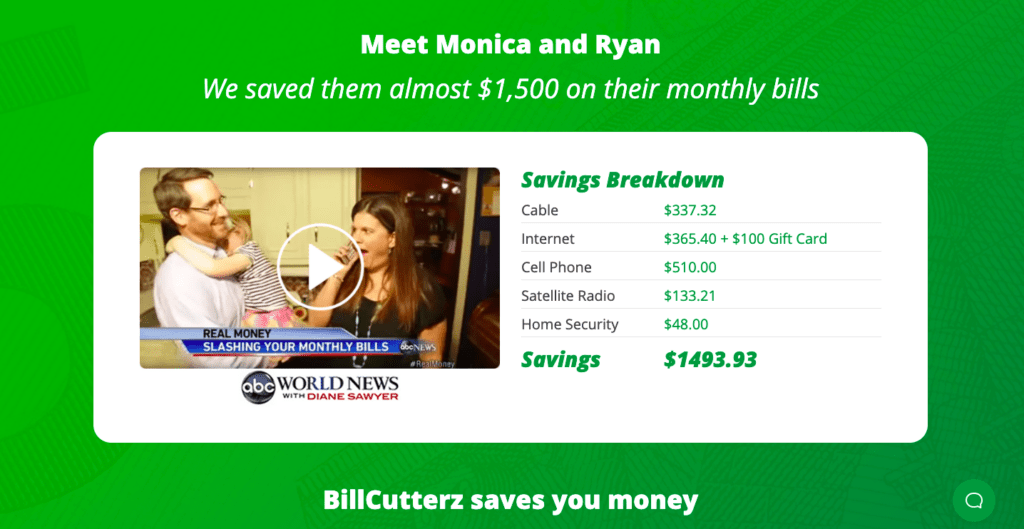

A service like BillCutterz can help you reduce your bills with no upfront payment necessary. If you want to find a way to lower your bills and save some cash, this company can help.

Here is how it works- BillCutterz will negotiate discounts for you with your service providers (cable, internet, security, etc.). If they manage to get a bill reduction, they take 50% of what they managed to save. If not, you pay nothing. So, if they save $100, they take $50 from what they manage to save you. Pretty simple, pretty fair.

Federal Student Loans

Also known as government loans, federal student loans are a type of funding designed to help guardians, students, and parents borrow money to pay for college. The federal government gives out these loans.

After you complete the FAFSA, the government can consider applicants for specific forms of financial aid. The guide used is the Expected Family Contribution margin. Thus it goes without saying that the sooner you can submit your FAFSA, the sooner more agencies will be able to qualify you for grants, subsidized federal student loans, and grants.

Keep in mind the difference in interest between subsidized and unsubsidized loans. The government covers the cost of interest for you in the case of subsidized loans. On the other hand, unsubsidized loans require you to cover all the interest costs, whether you are in school or deferment.

The three most popular types of federal student loans are:

- Direct Plus loans – these are mainly unsubsidized credit-based federal loans. These loans cater for college expenses up to attendance costs, usually, after your other financing is exhausted. The downside is that interest will be charged and capitalized, increasing your overall loan expenses.

- Direct subsidized loans – these are mainly awarded to students with financial needs and are highly federally regulated. No interest accrues while an undergrad attends school half the time at the minimum. In deferment periods, loan repayments are also postponed, albeit temporarily. There is also a six-month grace period after you leave school.

- Direct unsubsidized loans – these loans are not awarded based on financial need. Instead, each school determines what amount you can borrow based on attendance and the availability of other financial aid for students. A distinct point of note here is that interest will be charged during all periods, and unpaid interest is added to the principal loan amount (capitalization).

The benefits of federal student loans include flexibility of payments, salary-based repayment options, no need for cosigners, and no need for strong credit histories to qualify for such loans.

Private Student Loans

These are loans provided by banks, online lenders, and credit unions. There is no one-size-fits-all method for applying for private student loans. You have to apply at each lender until one agrees to fund your college education.

As always, your credit score will play a major role in how easily you land a private student loan. In many cases, it is necessary to repair one’s credit score before sourcing private student loans. A weak credit score may require a cosigner to help you get the financing that you need.

Since it is important to ensure you have a good credit score, you can use Credit Karma to figure out what your score is for free. The service also allows you to monitor your credit, get notified when there are changes to your credit report, monitor your ID for potential identity theft, and more.

One must read the terms and conditions thoroughly before signing the agreement. In particular, check if you need to make payments if you are enrolled half the time, what the fees are like, and if you will get a grace period.

Wrapping up how to find funding sources

The most comprehensive ways to fund a college education in the US include grants and scholarships, federal student loans, and private student loans. Alternatively, other ways to raise cash for college include changing schools, peer-to-peer lending, lowering your workload to part-time, and taking a gap year.

| Swagbucks pays you to take surveys online and is one of my favorite survey websites because of its countless survey options and trustworthiness. They pay you via PayPal or gift cards if you take surveys through their website. You also get a $5 welcome bonus using this link. | ||

| CIT Bank offers high yield savings accounts and term CDs that are great for people who are looking to invest their cash and earn interest. One of the reasons they are so famous among savers is because they have one of the nation’s top rates- 6x the national average (your typical savings account earns you just 0.09%). | ||

| FlexJobs is great if you are looking for remote work opportunities. The team at FlexJobs monitors every job posting to make sure the standard is maintained so you will find well-paying job opportunities and zero scammy ones. | ||

| For wise parents with their children’s futures in mind, an early tax-advantaged investment account specifically tailored for children is a fantastic idea. Programs such as UNest are designed to help you achieve this goal of crafting a better future for your children. |

||

| Credit Saint is my top pick when it comes to credit repair agencies. It has a 90-day money-back guarantee, an A+ rating from the BBB, affordable pricing and it has also been voted the best credit repair company by consumer advocate. Credit Saint |